Monthly Market Metrics | 09.2023

09/07/2023

Thank you for tuning in to Tungol Mandap’s Monthly Report on rates and economic activity affecting your real estate market today. The Monthly Market Metrics is a new series that will explore the things happening around us that affect the economics of buying a home. Often, people miss opportunities in the real estate market because they are looking at the wrong aspect or they don’t see how valuable a compromise can be. Hopefully, this report will help you make some informed decisions about home-buying at the right time. Our contributing lending expert, Mark Thatcher of Fairway Independent Mortgage Corp., will break things down in ways that are easy to understand and hard to forget, so you will have a toolkit of knowledge to interpret things you hear about the real estate market.

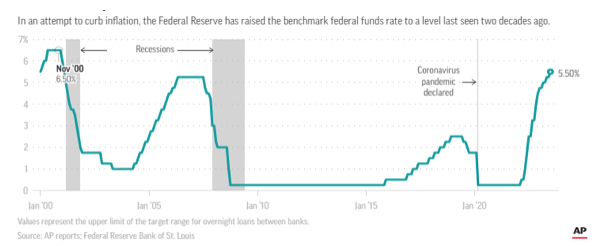

We stated in last month’s report that the Federal Reserve does not establish the interest rates for consumers to buy homes. Many people think that when the Federal Reserve, often referred to as “the Fed,” raises the Federal Funds Rate, they are raising the interest rates on home mortgages. They are not. Commercial banks are required by law to keep a certain amount of money in accounts at Federal Reserve banks that would allow them to cover their depositors' withdrawals. Anything over this amount, banks are allowed to lend to other banks. When a bank lends money to another bank, they charge them interest. That interest rate is the Federal Funds Rate.

If you’re wondering now who establishes mortgage rates, we could say that each individual lender does. And what influences their decisions each day? The simplest answer is… Market Forces. To be a little less vague and dramatic, though, we can review what we said last month, which is that mortgage rates tend to track the 10-year treasury yield. However, mortgage lenders consider what the Fed is doing, along with the rate of inflation, supply and demand, and the secondary mortgage market when setting fixed rates.

So we know that lenders do consider what the Fed is up to when it sets the fed funds rate, but we also know that this is only a piece of the puzzle. Economists are somewhat mixed right now about whether they think the fed funds rate will change at the next meeting of the Federal Open Market Committee (FOMC) from Sep 19-20. Did you just wonder who the FOMC is? They are the committee within the Federal Reserve who decide what to do in the open market to reach the goals of the US government’s monetary policy. Keeping the prices down of all the things we buy has been a major priority. https://www.federalreserve.gov/monetarypolicy/fomc.htm

The Case-Shiller Home Price Index measures appreciation or the amount that home prices rise. From May to June, the index said home prices rose 0.7%, which was the 5th month of consecutive gains. People often ask me if I think now is a good time to buy a home. We can look at this index and say that based on the fact that home prices have been rising, if you wait, you will end up paying more for your house than you would have 6 months or a year earlier. But what if interest rates are higher today than they were 2 years ago? Would it be a good idea to wait until rates are lower? You might think that there is a controversy in answering this question, but let’s reframe the question so that we can come up with a clear answer. Would I be in a better financial position if I bought a home now and then refinanced the mortgage once rates dropped or should I wait to buy a home when rates are lower?

A person buying today might be offered a rate that is close to the national average rate surveyed by Freddie Mac recently*. If they bought a home for $500,000 with a 3% down payment at a rate of 7.125%, the loan amount would be $485,000, and the principal and interest portion of their payment would be $3,267. In 12 months, we can imagine that rates are down to 5%. At this point, the loan amount is lower, but you might roll in your closing costs, so the loan amount after only a year of payments could be about the same as your original loan amount. The payment drops to $2,603.

What would your payment be if you waited that year to buy at the lower rate? The same home 12 months later could appreciate to a price of $540,000 if we use an 8% annual appreciation rate. Your down payment and loan amount will be higher. With a loan amount of $523,800 and an interest rate of 5%, the monthly payment is $2,811. So even though rates went down significantly in that year, you end up with a higher loan amount and a higher monthly payment of $208. Buying today wins the day.

Since March of last year, the Fed has increased the Fed Funds Rate 11 times, including the hike from last Wednesday. The Fed Funds Rate is the interest rate for overnight borrowing for banks. Mortgage rates don’t mirror the Fed Funds Rate. They tend to track the 10-year treasury yield. However, mortgage lenders consider what the Fed is doing, along with the rate of inflation, supply and demand, and the secondary mortgage market when setting fixed rates. Fed Chair Jerome Powell wouldn’t say whether they planned to increase rates again at the next meeting in September.

Pending Home Sales rose 0.3% from May to June. This was the first increase since February. Sales are down 16% from a year ago, but this is largely due to a lack of inventory. Pending Home Sales measure signed contracts on existing homes, which is about 90% of the market and is considered a forward-looking indicator of home sales. Lawrence Yun, chief economist for the National Association of REALTORS (NAR), explained, “The presence of multiple offers implies that housing demand is not being satisfied due to a lack of supply. Homebuilders are ramping up production and hiring workers.” If we had more homes for sale, we would have a higher rate of signed contracts! https://www.nar.realtor/newsroom/pending-home-sales-rose-0-3-in-june-first-increase-in-four-months

Report Provided by Mark Thatcher, Fairway Mortgage Corp.

Mark Thatcher, NMLS #1883412

Tel: 202-394-8469

Email: mark.thatcher@fairwaymc.com

In Search for Your Home? Apply Today: Click Here